Venture Capital in Latin America: Connecting Opportunities

Venture capital (VC) in Latin America is a new industry that has shown a remarkable evolution since the early 2000s. In countries with some VC activity, development agencies, NGOs, and the government have played a strong role in promoting entrepreneurship, innovation, and the first breed of VC managers. Given their developing economies, these countries and their entrepreneurs and managers are still in exploration mode regarding how to create, finance, and globally grow high-potential companies.

When analyzing VC in Latin America, most of the structural elements found in the U.S. market need to be revised. Entrepreneurship is still in its infancy in many countries and there is a lack of institutional investors willing to invest in VC—an industry barely known to them—which leaves VC managers and funds with limited options to raise money. The pipeline of potential investments with high growth profiles is not abundant and local exit strategies are almost non-existent.

Given this reality, is there really an opportunity to do venture capital in Latin America? We faced this question in 2008 when we founded Austral Capital—would we be able to find entrepreneurial talent, global opportunities, investors, and exits in a country like Chile with its population of only 17 million?

At the time, I was fortunate to have just spent five years as Managing Director of Endeavor in Chile, a global organization that promotes high-impact entrepreneurship in emerging markets. From that position I had witnessed the challenges, barriers, and opportunities that Latin American entrepreneurs face in building their companies, raising money, and thinking globally. My conclusion at the time was that talent existed in abundance but it was not enough to build successful companies.

In this article, I provide some context on the region and the industry before describing the major opportunities and challenges for venture capital in Latin America. The article closes by describing key elements of a model for investing regionally.

Entrepreneurs in Latin America

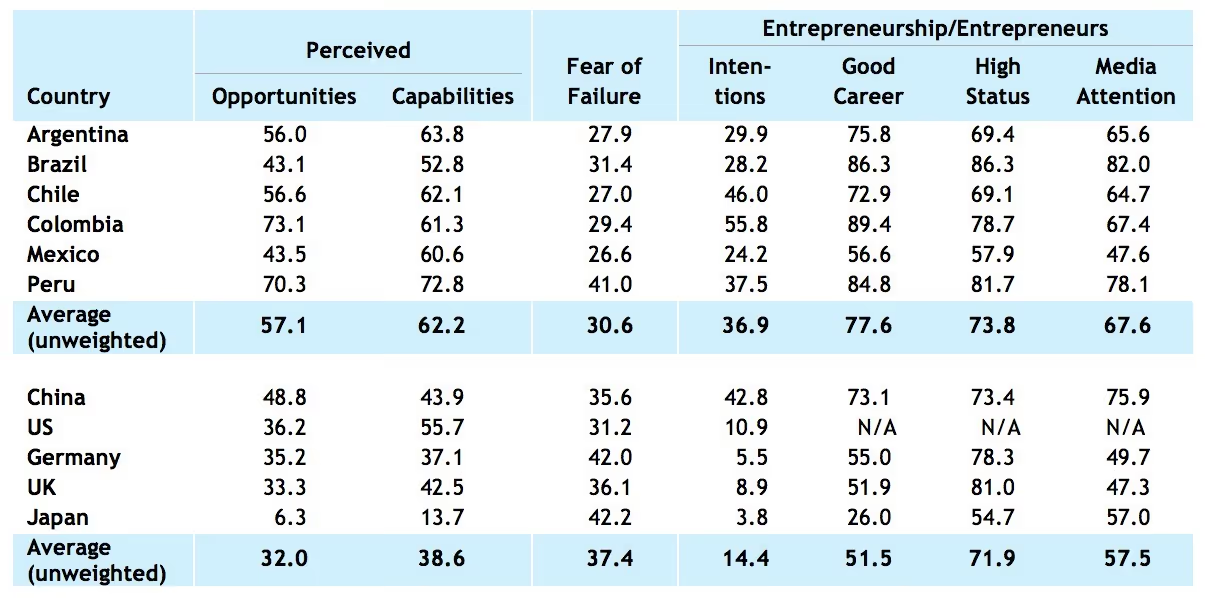

The particulars of entrepreneurial activity depend on the country being analyzed. According to the 2011 Global Report from GEM,1 Latin American countries differ highly from developed economies and among themselves in terms of potential entrepreneurs. To analyze this potential, the GEM study explored three societal attitudes: perceptions about entrepreneurship as a career choice, the status of entrepreneurs, and the media attention they receive.

As shown in figure 1, the average perceived opportunities, perceived capabilities, and entrepreneurial intentions in Latin American countries2 are significantly higher than those shown in developed countries.3 According to the GEM report, among Latin American countries, Brazil and México show the lowest levels in opportunities, capabilities, and intentions compared to Chile, Colombia, and Perú.4 In terms of Entrepreneurship as a Good Career Choice and High Status to Successful Entrepreneurs, Brazil, Colombia and Perú show the highest index and México the lowest one in the group analyzed.

Figure 1. Entrepreneurial Perceptions, Intentions, and Societal Attitudes (in percentage of population aged 18-64).

Author’s image; data from Kelley et al., 2011 Global Report, 7-9. Score represents percentage of population aged 18-64.

For many years, institutions like Endeavor have spent time and resources in Latin America in order to understand the main challenges that face local entrepreneurs. According to Endeavor’s experience, several factors affect entrepreneurship in these countries, including the following:

- cost of failure,

- limited management expertise,

- lack of contacts or mentors,

- lack of trust,

- limited access to smart capital, and

- lack of role models.5

Among these factors, Endeavor pays special attention to role models—entrepreneurs who will eventually help to inspire others to start companies. Two entrepreneurial teams stand out who have been able to scale their businesses globally and attract investors: Marcos Galperin from Mercado Libre6; and Martín Migoya, Martín Umaran, Néstor Nocetti, and Guibert Englebienne from Globant. Marcos Galperin has also been successful in listing his company in the United States. Both companies started in Argentina and in both cases the entrepreneurs built successful companies that are likely to last, becoming some of the best role models for the region to date.

Local Context Matters

When analyzing different countries in Latin America, local context significantly affects the capacity of entrepreneurs, investors, managers, and other stakeholders in the process of building successful companies. For example, it is useful to compare aspects such as perceived corruption, protection of minority shareholder rights, protection of intellectual property rights, capital market development, corporate government requirements, and use of international accounting standards.

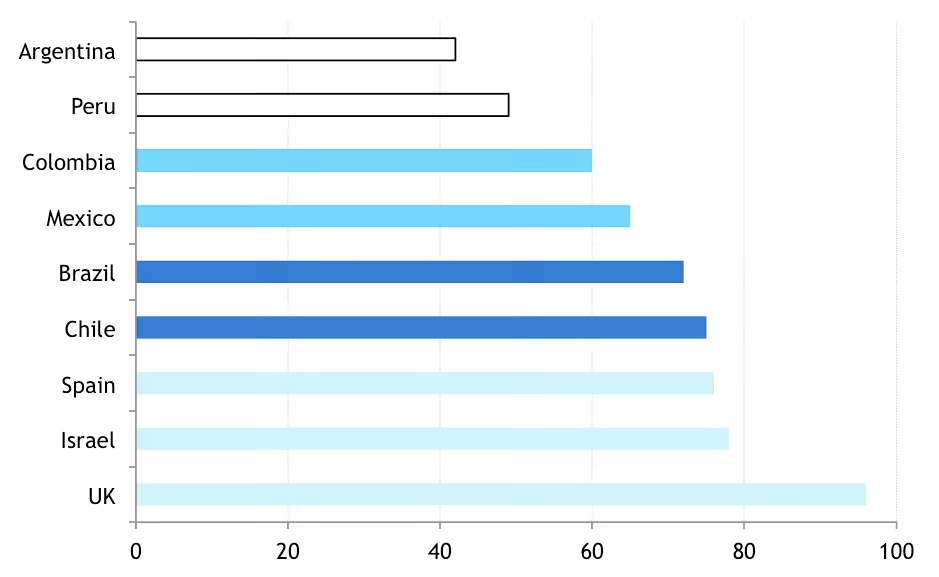

Since 2006, the Latin American Venture Capital Association has analyzed the above factors in order to rank Latin American countries in terms of their attractiveness for venture capital and private equity. Figure 2 presents the key data reported in 2012.

Figure 2. Overall Scores for Private Equity and Venture Capital Markets 2012, by Latin American Venture Capital Association Ranking.

Author’s image; data from the Latin American Private Equity and Venture Capital Association, 2012 Scorecard, page 4. Overall scores range from 0 to 100, where 100 equals the best/strongest environment.

In figure 2, three groupings of Latin American countries can be seen. The first group—Brazil and Chile—shows strong market conditions for venture capital and private equity, comparable to countries like Israel and Spain. When looking at detailed information for 2012, Brazil’s strength lies in its regulatory framework for fund formation, and its challenges are mostly related to the perception of corruption and the low level of protection for intellectual property rights. Chile’s strength is related to the low level of perceived corruption, and its challenges are related mostly to certain restrictions on local institutional investors.7

The second group is comprised of Colombia and México. Again looking at 2012 data provided by LAVCA,8 Colombia’s strengths are the protection of minority shareholder rights, fund formation, and the potential to restrict institutional investors; the country faces challenges in perceived corruption and the implementation of international accounting standards. México’s strengths are related to tax treatment, corporate governance, protection of minority shareholder rights, and restrictions on local institutional investors; its challenges are related to an inefficient judicial system and negative perception of corruption.

Argentina and Perú compose the third group. Argentina shows one of the strongest entrepreneurial communities in the region, with its main challenges being lack of a regulatory framework, legal uncertainty, underdeveloped capital markets, and a complex tax environment. Perú scores positively on inward investing and corporate governance, with the country’s main challenges related to corruption, a weak judicial system, tax treatment, and the protection of minority shareholder rights.9

Investors in Latin America

Historically, it has been difficult to attract investors to the VC industry in Latin America, for a number of reasons: the different country contexts described above, the lack of a track record of established VC firms in Latin America, the nascent but still “globally” immature new generation of entrepreneurs, and the scarcity of exit strategies in the region. Despite this reality, some key institutions (both global and local) have been strong promoters of the development of the VC industry by directly investing in the very first venture capital funds in the region.

In a regional context, the Multilateral Investment Fund (MIF)10 invested in 50 funds regionally between 1996 and 2010, committing $220 million to seed funds all over the region. By bringing credibility as an investor, the goal of the MIF’s venture capital program has been both to support first-time VC managers and also to help attract private investors to these funds.11 Other institutions that have played key roles in this respect are the Development Bank of Latin America (CAF) in the Andean region, Brazilian Development Bank (BNDES), and Chilean Innovation Development Agency (CORFO)—all providing investments to emerging funds, in the form of both equity and loans.

On the private side, pension funds, endowments, insurance companies, family offices, and wealthy individuals have naturally been the target of the new breed of VC managers in the region. Among this group, the role of pension funds and insurance companies investing in VC funds has been limited but is increasingly active in countries like Brazil, Colombia, and most recently, México.

In this context, family offices and wealthy individuals have become one of the primary sources of funds for VC in the region. This trend involves a new series of challenges, as some private investors tend to look for control not only at the portfolio-company level but also at the fund-manager level, making it difficult to emulate the traditional VC structure, promote entrepreneurs, and have fully independent VC managers.

Exit Strategies

Back in 2008, the U.S. National Venture Capital Association published a news release titled “IPO Drought Creates Capital Market Crisis for Start-Up Community,”12 referring to the fact that no venture-backed U.S. IPOs had been issued in the second quarter of 2008 and only five during the first quarter. Newsworthy as that may be in the United States, this situation is a permanent reality for Latin America where the IPO market is almost non-existent for venture-backed companies.

Most VC funds in the region originally sought exit options outside the public markets. In their search for feasible exit strategies, some fund managers have followed an approach based on local and regional strategic sales; on very few occasions, they have been able to sell companies to U.S.-based players. Without a doubt, the lack of exit markets is one of the main challenges for venture capital in Latin America.

Austral Capital’s Approach

When Austral Capital started operations in Chile in 2008, we knew that staying local was not the right decision. Between the smaller, local market and the non-existent exit options, we decided to invest in local companies that we believed could compete abroad, mainly in the United States and Brazil.

This decision raised many questions. Was the quality of Chilean entrepreneurs sufficient to compete in those markets? How could we help them in markets where we had no presence? How would the entrepreneurs’ performance be affected by the fact that they were supposed to eventually move abroad? Would our portfolio companies be able to attract coinvestors from these markets? The list of uncertainties was virtually endless.

As we considered these and other questions over the early months, we finally decided to open a small office in California at the end of 2008. For the next four years, each Austral Capital partner spent on average one week per month in California, not only helping our portfolio companies to start operations in the United States but also relating to other VC managers, technology companies, and universities in order to be effective in the support we provided to our portfolio companies.

This strategy paid off for Austral Capital. By mid-2012, Austral Capital portfolio companies had been able to attract top VC investors, including Sequoia, Motorola Ventures, Madrona, and Xseed, among others.

Venture Capital Opportunity in Latin America Today

For the last several years, we have analyzed how to take advantage of the enormous entrepreneurial talent in Latin America under a venture capital model. Interestingly, the question of whether it makes sense to have a regional VC fund remains unanswered for many VC managers in Latin America. We at Austral Capital believe so.

In this context, a recent study undertaken by Austral Capital analyzed five Latin American countries and their potential for venture capital, including parameters such as the availability of tech and biotech startups and support from the local government. The results of this study are summarized in figure 3.

Figure 3. Venture Capital Analysis of Latin America Countries.

Austral Capital’s image, used with permission; data from country analysis, third-party reports, and direct interviews with key local players.

As figure 3 reflects, Brazil excels in dealflow, market size, limited partner base, and overall support to the industry, and probably has the most dynamic industry in the region. Chile shows a strong supporting environment for the industry, including government programs to promote the creation of new VC funds and Start-up Chile, an ambitious program to attract entrepreneurs to the country. Colombia represents a new market with good potential and very few players. México shows remarkable activity in the last few years, having both an active private and public sector promoting the industry. Finally, Argentina presents a very active entrepreneurial community but a very complex local business environment.

A Model to Invest Regionally: Connecting Opportunities

In our work at Austral Capital, we have witnessed business opportunities in most Latin American countries that, if supported and connected adequately, could become success stories for the industry as a whole. Therefore, we advocate for a regional investment model where talent, capital, and markets can be connected.

When developing a model to invest regionally, at least two factors should be considered carefully. First, VC remains a local business, so any global strategy should consider a local presence in the markets of interest. Second, exit strategies should be at the center of the analyses—not because dealflow, regulations, and local contexts are not challenging, but because in our opinion exits are the factor most underestimated by VC managers in the region.

The United States is the single most active market in terms of venture capital deals, and Latin American entrepreneurs and technologies have been demonstrated as attractive and competitive in the U.S. market—when they have the right partners, capital structure, and strategy. Therefore, we believe that a successful venture capital regional model needs to be based on exits in the United States, connecting technologies, entrepreneurs, and investors in a model that is able to generate high growth-potential companies that start in the Latin American region but can compete in the United States.

If this approach is adopted, however, there are several immediate questions. First, given the diversity of countries and locations, how can one detect the best entrepreneurs in the region? We have analyzed different models that both VC and private equity firms have used in the region, from a regional fund approach, Satellite Local Funds, local partner funds, and regional club alliances. We found that regardless of the model used to develop a presence in the region, VC partnerships must count on full-time local partners who know and understand the local context and the complexities of the country where they are based.

Second, once entrepreneurs have been found, how can one connect opportunities in Latin America with the U.S. market? For many years, entrepreneurs and investors have thought that spending sporadic time in the United States would eventually help them “be part of the system” and thus enable them to get investments, business partners, and successful companies. In our experience since 2008, to be able to connect to U.S. opportunities, there needs to be a very high, permanent level of commitment (both financial and personal) to being in the United States. Only spending enough time in the market of interest (i.e., the United States) triggers the connecting opportunities that otherwise would not be available.

Looking Forward: The Potential of Latin American VC Opportunities

In a world where other regions are facing challenging times, Latin America appears as a growing market for many industries, including venture capital. The fact that many VC firms in the United States are looking for exposure in this region opens a new set of opportunities for Latin American VC managers looking for the right U.S. partners under the regional approach proposed in this article.

Despite all the challenges of the industry, VC in Latin America seems to be at its highest point ever, because of both the level of entrepreneurial activity and the rise of new VC funds and managers who are starting to think globally. Whether the technologies come from Latin America or the United States; whether entrepreneurs are Chilean, Brazilian, or Colombian; whether investors are located in México or Argentina—”Think big, stay connected, and partner with the best” seems to be the right strategy for successful venture capital in this young region.

Gonzalo Miranda

Gonzalo is Founding Partner of Austral Capital Partners, a venture capital firm based in Santiago, Chile. Austral Capital invests in different industries, including technology, life sciences, natural resources, and energy in Latin America and the United States. Prior to founding Austral, Gonzalo was Managing Director of Endeavor Chile, a global organization that promotes high-impact entrepreneurship in emerging markets. He currently holds board positions at ACAFI (Chilean Fund Managers’ Association), Scopix, Paperless, Multicaja, Indef, Producto Protegido, and Chile Patrimonial (nonprofit). Golzalo holds a BSc and MSc in mechanical engineering from Universidad Católica de Chile and an MBA and MOT (Management of Technology) from the University of California, Berkeley.

1 Donna J. Kelley, Slavica Singer, and Mike Herrington, GEM 2011 Global Report (Global Entrepreneurship Monitor, 2012).

2 Includes Argentina, Brazil, Chile, Colombia, México, and Perú.

3 Includes China, the United States, Germany, the United Kingdom, and Japan.

4 Kelley et al., GEM 2011 Global Report.

5 Endeavor Global, Impact Report 2010–2011 (2011).

6 (MELI) Stock Quote at NASDAQ.

7 Latin American Private Equity and Venture Capital Association (LAVCA), 2012 Scorecard (2012), 8–11.

8 Ibid., 12–13, 20–21.

9 Ibid., 6–7, 24–25.

10 A member of the International Development Bank group.

11 Susana Garcia-Robles, “Venture Capital at the MIF: Empowering SMEs and Entrepreneurs in Latin America and the Caribbean,” presentation at FOMIN, March 2010.

12 Channa Luma, Sandy Anglin, and Matthew Toole, “No Venture-Backed IPOs Issued in the Second Quarter of 2008: IPO Drought Creates Capital Market Crisis for Start-Up Community” (news release), Thomson Reuters and National Venture Capital Association, 1 July 2008.